Record High US Long-Term Interest Rates

Reckless US fiscal policy is pushing up long-term US interest rates to record levels

The ratings agency Moody’s downgraded US government debt on Friday. The downgrade itself isn’t exactly news. After all, it’s well known that US fiscal policy has been on an unsustainable path for a long time. But the downgrade is adding to upward pressure on longer-term yields today, exacerbating a trend that’s seen long-term yields rise sharply for quite some time. Higher yields make it more expensive for the US to issue debt, adding urgency to the need to get our fiscal house in order. I’ll devote this week’s posts to US government debt, starting with a look at long-term yields today.

The benchmark interest rate for US government debt is the 10-year yield. That tenor is incredibly important, as it feeds into everything else in our economy, including mortgage rates and loans to companies. If you just look at 10-year yield, this now stands at 4.5 percent, which doesn’t look too alarming. After all, this yield stood at 4.8 percent in January just before the inauguration. But - under the hood - worrying things are happening, which I focus on now.

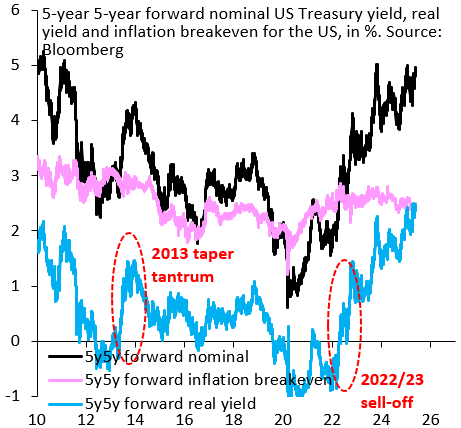

You can break down nominal US interest rates into market expectations for inflation - what’s called breakeven inflation - and the real interest rate, a residual that’s left when you subtract breakeven inflation from the nominal yield. The chart above shows these three things, with one added twist. It does this decomposition for 5y5y forward yield, which is the second half of the 10-year yield when you take out the “front-end” 5-year interest rate. This perspective shines a light on longer-term interest rates, which are so important for US debt sustainability. This is where recent trends are worrying.

The 5y5y forward real interest rate (blue line) now stands at 2.5 percent, which is the highest level going all the way back to 2010. Most importantly, it far exceeds levels seen during hawkish Fed episodes, like the 2013 “taper tantrum” or the 2022/23 hiking cycle after the COVID inflation scare. If anything, the Fed is now contemplating further cuts as the economy weakens, weighed down by tariffs, so the fact that real long-term interest rates are rising at this juncture is highly unusual and worrying.

It’s worth noting that 5y5y forward breakeven inflation (pink line) is well-behaved and stable around 2.5 percent, so this isn’t a story about Fed credibility amid a tariff inflation scare. That makes it all the more likely that many years of irresponsible fiscal policy are catching up with the US, adding urgency to the need to get our fiscal house in order.

The 30-year Treasury yield is flirting dangerously with the 5% threshold. Interest rates are not just raw numbers: they are signals, messages, clear indicators. An episode of stress similar to what the UK experienced in October 2022 cannot be ruled out. In this case, however, it would affect the world’s reserve currency and the ultimate risk-free asset. The consequences could be nonlinear.

If willing to cause inflation or a recession, maybe the game could go on a long long time (Japan 1989)