Turkey's Huge External Imbalance

The "core" trade deficit - excluding gold and energy - is as wide as it's ever been

Back in November, I wrote a post about how Erdogan abuses Turkey’s banking system to engineer one credit boom after another. His goal is to run the economy “hot” into elections - cementing his grip on power - but the imbalances this creates are massive. The fact that the economy is constantly operating above potential means imports are far too high, which is why Turkey has a chronic - and large - current account deficit. This deficit periodically sparks currency crises and hyperinflation.

The current account deficit is therefore the single most important variable to monitor for Turkey, essentially because it measures the gap between Erdogan’s aspirations and reality. Today’s post look at the latest data. When you exclude gold and energy, this deficit has widened back to levels that - in the past - proved unsustainable and sparked currency crises.

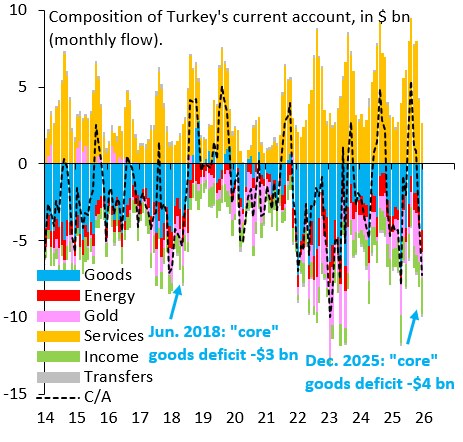

The chart above shows the composition of Turkey’s current account deficit. I’m interested in the blue bars, which are what I consider the “core” current account deficit. The idea is similar to core inflation, which aims to measure underlying inflation by excluding noisy categories like food and energy. In the case of Turkey’s current account, noise comes from energy imports (red bars) - since fluctuations in oil and gas prices can be erratic - and gold imports (pink bars), which households lean on increasingly to protect their savings from currency devaluation and inflation. You can think of the blue bars as the “core” goods trade deficit.

In the most recent data for December 2025, this “core” deficit is wider than it was just ahead of the Balance of Payments (BoP) “sudden stop” in August 2018, which resulted in a massive Lira devaluation. Turkey is back in the same danger zone it’s been in for the past decade. The reason is Erdogan’s weak grip on power, which means he has no choice but to goose growth artificially. Wide current account deficits are the result.

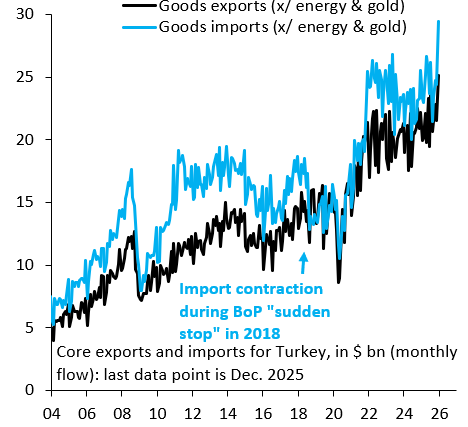

The chart above shows what’s going on with “core” goods trade. The black line is exports excluding energy and gold. The blue line is imports excluding both of these categories. The difference between these two series - exports minus imports - is the blue bars in the first chart. The December 2025 data point shows a big spike in “core” imports, the likes of which Turkey hasn’t seen since the massive credit stimulus that took place during COVID. This kind of import spike always ends the same way for Turkey: Lira devaluation.

The consequences of creating a false balance with a strong lira.

Thats not how current accounts work though lol you can’t just strip out components you don’t like and say “see how much worse it is”, you’re also talking about a absolute numbers (billions) rather than percentage of gdp/trade, which normalizes across time periods. Very weird article for an economist