What the fall in the Dollar is and isn't

Recent data have pulled the Dollar lower, underscoring that its decline is cyclical

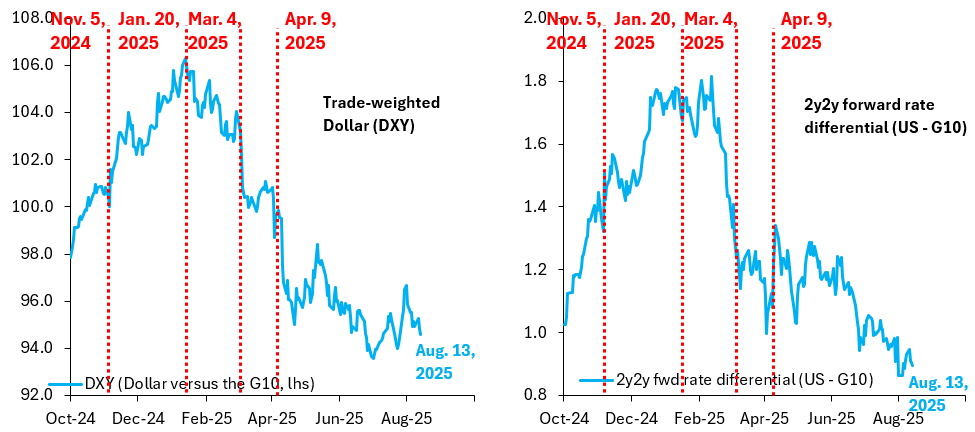

A lot has been written about the Dollar, which is down 10 percent on a trade-weighted basis against its peers. One of the biggest debates is around whether its fall is cyclical, i.e. due to temporary factors, or structural as markets question reserve currency status. The most recent fall - in the wake of large downward revisions to payrolls and a tepid CPI inflation print - helps shed light on what’s going on. It underscores that markets are basically trading the short term data flow, which means the fall in the Dollar is cyclical. It isn’t about a loss in reserve currency status or structural damage.

The left chart above shows the most widely-used Dollar index - the DXY - which measures the strength of the Dollar against its G10 peers. The right chart is the accompanying interest rate differential, where I am looking at a trade-weighted 2y2y forward interest differential (US - G10) using the same trade weights as the DXY.

After big falls around tariff announcements in February and April, the Dollar has essentially been flat since May. Following large downward revisions to payrolls and this week’s tepid CPI print, which showed tariff passthrough slowing, the Dollar has fallen sharply, which underscores that markets are trading data, not structural things like reserve currency status.

The key issue now - which is what rate differentials capture - is how much the Fed will ease relative to other G10 central banks. In the wake of recent data revisions and the CPI, 69 bps in cuts are priced for the remainder of 2025, so almost three 25 basis point cuts. That seems like too much to me given that underlying inflation is clearly picking up, even as lots of uncertainty remains about tariff passthrough.

Pensará lo mismo Stephen Minar próximo camdidato a dirigir la FED ?

Según parece, no.