The Global Rise in Long-Term Yields

Out-of-control fiscal policy is driving longer-term yields up everywhere

My two posts so far this week have focused on the US and the role that out-of-control fiscal policy is playing in driving up long-term Treasury yields. There’s certainly a lot to lament about the US in this regard, but the truth is that fiscal policy is seriously out of whack in many places. Today’s post looks at this global dimension and the role it’s playing in pushing up long-term Treasury yields.

In the decade after the global financial crisis, inflation was stubbornly low across all major economies. This encouraged the illusion that interest rates would always be low, no matter how much debt governments ran up. This thinking informed global policy making when the pandemic hit. Governments everywhere ran much bigger deficits than ever before and global indebtedness rose sharply. Encouraged by the illusion that interest rates would always be low, governments after the pandemic never got deficits back under control, with debt issuance everywhere remaining far bigger than before COVID. This recklessness is now haunting the world.

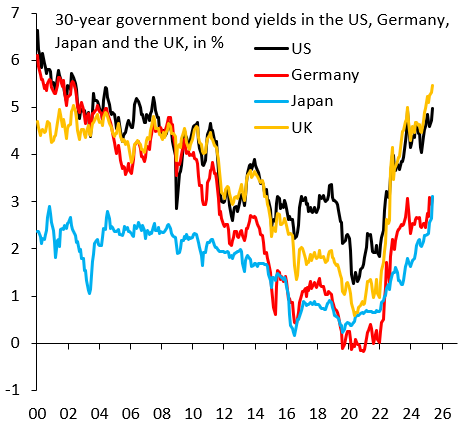

As I discussed in yesterday’s post, it’s the very long end of the yield curve where risk premia are most important. That’s why I look at the 30-year government bond yield in the US (black), Germany (red), Japan (blue) and the UK (orange). Long-term yields in the US are up, but the truth is that what’s going on in the US is modest compared to the UK or Japan, where - in both cases - the 30-year yield is now at its highest level going back all the way to 2000. The global debt binge during and after COVID is now exacting a price, with global yields rising sharply. Poor fiscal policy is a global problem, not just a US problem.

A final word on Japan, where the recent rise in the 30-year yield is quite shocking. This rise obviously exacerbates whatever rise is already happening in US yields. When Japanese bond yields were low, this encouraged Japanese households to seek higher yields overseas. Some of the resulting capital outflow from Japan went into US Treasuries, helping keep longer-term US interest rates low. With the sharp rise in Japan’s 30-year yield, this dynamic is now much less, which adds to upward pressure on longer-term US yields. In effect, the rise in Japanese interest rates is exporting Japan’s high debt level to the rest of the world.