The Relationship Between The Dollar And Oil

USD used to have a negative correlation with oil prices, but shale has made it positive

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

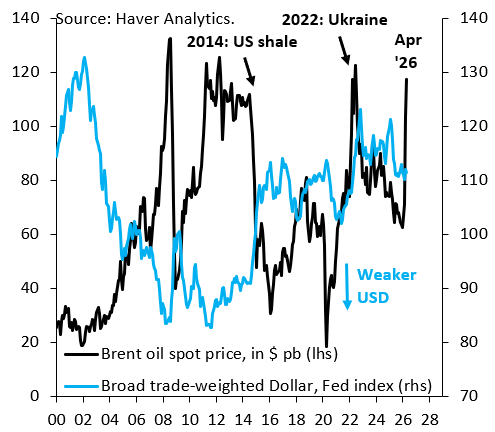

Historically, the Dollar has been thought of as having a negative correlation with oil prices. The rationalization for this was that higher prices tend to widen the current account deficit, which in turn should drag the Dollar down. This might have applied before shale drilling transformed the US into the world’s biggest oil producer, but it certainly no longer holds now. After all, the US has become a net exporter of oil over the past five years, so rising oil prices should - at the margin - lift the Dollar. That’s indeed what we see in the data. The correlation between the Dollar and oil has become slightly positive in recent years.

The blue line in the chart above is the Federal Reserve’s trade-weighted index for the broad Dollar, while the black line is the Dated Brent “spot” oil price. Going back to the early years in the chart, there’s a negative relationship between the Dollar and oil, like before the 2008 crisis (when “peak” oil weighed on the Dollar), during the height of the crisis (when oil prices tumbled and the Dollar rose) and in its aftermath (when oil rose and the Dollar fell). But - more recently - there’s a positive correlation, which sees the Dollar and oil move together. This kind of correlation shift begs the question whether it’s spurious or rooted in some kind of structural change in the economy. In this case, it’s the latter. The structural change is the emergence of shale oil as a massive phenomenon about a decade ago.

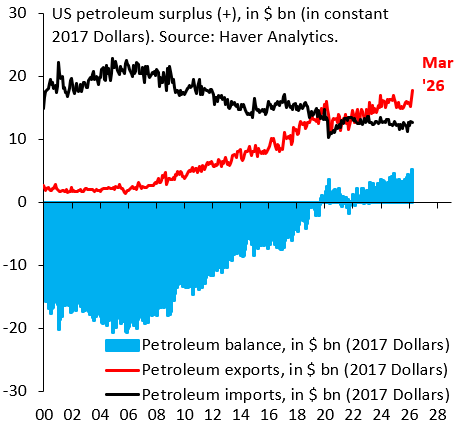

The blue bars in the chart above show the petroleum balance for the US in constant 2017 Dollars. The black and red lines are the corresponding export and import series. What’s clear is that the US has undergone a profound change over the past decade: it’s shifted from being a net importer to being a net exporter. So the shift from a negative correlation of the Dollar with oil to positive makes sense. There’s certainly no reason to think it’s spurious.

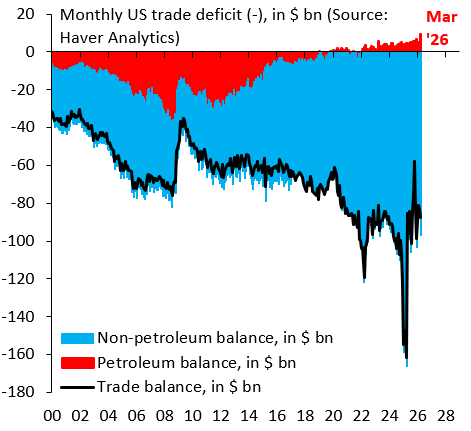

At the same time, it’s important not to make too much of this. The chart above shows the overall trade deficit (black line), of which the petroleum balance (red bars) - now in surplus - is just a small part. The US has become a net exporter, but - in the scheme of things - it’s a small one because most of the domestically produced oil is consumed at home. The bottom line is that a genuine structural shift has happened, but it’s small fry for the Dollar, which remains primarily a function of rate differentials as a proxy for all the things that drive monetary policy vis-à-vis the rest of the G10.

The fact that the correlation of the Dollar with oil is now slightly positive supports my Dollar down view for this year. I expect oil prices to fall back to the status quo ex ante once the Strait of Hormuz reopens, which - at the margin - will weigh on the Dollar.

Thank you for your posts over the last couple of months. They're very informative. However, I'm dubious that the Strait of Hormuz will be reopening anytime soon, no matter what the effect on the Iranian or worldwide economy. This is turning into a geopolitical quagmire from which there appears to be no escape.

I wonder if the new net oil exports is so small a matter. Figures from 2023 that I've seen put oil as a sixth of total exports by the US of that year. The US is threatened with the loss of this export by the transition to renewables -one reason I suspect for the hostility of the current administration to renewables. But how big an effect will all this have for the dollar - the loss of this new net export could be of considerable effect on morale I would think. Ian