Turkey falls back into crisis

Only very large FX intervention has stopped the Lira from tumbling - that can't last

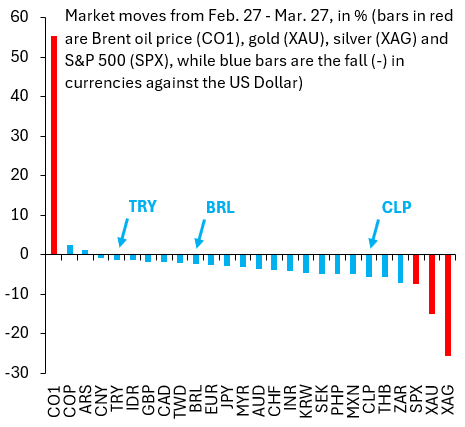

When the war with Iran started just over a month ago, I wrote a series of posts about how markets would trade this shock, using price action from the weeks after Russia’s invasion of Ukraine as a guide. Back in 2022, oil prices rose sharply because markets feared an embargo of Russian oil, lifting currencies of oil and commodity exporters and weighing on commodity importers. Biggest beneficiary was the Brazilian Real, while the Turkish Lira got hammered.

This isn’t how things have played out now. In fact, the opposite has been true. The chart above shows how different asset prices have moved between Feb. 27 and Mar. 27. The red bars show the large rise in Brent (CO1), the fall in the S&P 500 (SPX) and the big drop in gold (XAU) and silver (XAG) prices. The blue bars show how different currencies have traded against the Dollar. A negative number means that a currency has fallen against the Dollar, while a positive number means it’s risen. The remarkable thing is that the Turkish Lira (TRY) has done better than Brazil’s Real or the Chilean Peso (CLP), to name just two commodity exporters.

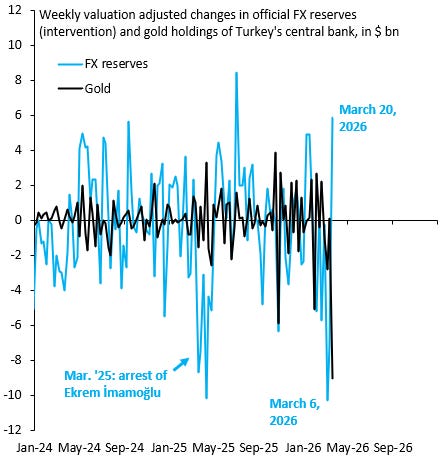

The chart above shows why the Turkish Lira has been resilient. The blue line shows my proxy for weekly intervention in the foreign exchange market by Turkey’s central bank. When this number is negative, it means the central bank is selling Dollars to lift the Lira. When it’s positive, the central bank is buying Dollars to slow appreciation of the Lira. The black line is the change in the central bank’s gold holdings. A negative number signals a drop, while a positive number means a rise. Both series are adjusted for valuation effects, so - in the case of gold for example - I adjust for the rise and fall in the price of gold over time.

Two points are worth making. First, since the outbreak of hostilities, intervention to support the Lira has been at least as big as during the crisis in March 2025, when the arrest of Ekrem İmamoğlu - the leader of the opposition - sparked huge capital flight. Second, the surprising rise in official FX reserves in the most recent data point for the week ending March 20 is explained by the drop in gold holdings, which I wrote about yesterday. The central bank sold and swapped 50 tons of gold for a value of around $8 billion Dollars. The fact that official FX reserves rose only about $5 billion adjusting for FX valuation effects means reserve losses continued unabated. The bottom line is that the Lira is under big depreciation pressure and - much like in March 2025 - the government will end up capitulating.

The basic problem in Turkey is Erdogan. To stay in power, he runs the economy hotter than is sustainable, using banks to engineer one credit bubble after another. That widens out the current account deficit and leads to one currency crisis after another. The catalyst for these crises is always an external shock. This time around it’s the war in the Persian Gulf and the associated spike in oil prices.

But how can you be so sure that devaluation of the Turkish Lira is a bad thing overall? It decimates saving sure, but helps wipe out debts, and make exports cheaper and imports more expensive.

What all this instability does do is hurt business planning, and that perhaps is the biggest minus. But by how much?

Need much more information I submit to come to easy conclusions, though I agree with you that Erdogan is the problem. Ian

Great job, Robin!