What Should Japan Do?

An imagined conversation on Japan with my friends Brad Setser and Joe Gagnon

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

I thought I’d do something a little bit different today. I’m going to give my diagnosis of what I think is wrong with Japan and what - therefore - needs to be done to lift the country out of its current debt trap. I’ll then contrast my views with those of two good friends: Brad Setser from the Council on Foreign Relations in NY and Joe Gagnon from the Peterson Institute in DC. The big picture on Japan is complex and there’s plenty of room for reasonable people to disagree. So I’m contrasting their views - I apologize in advance for anything I screw up - mainly to highlight where I see things differently, which I think is quite instructive for debating Japan and what needs to happen.

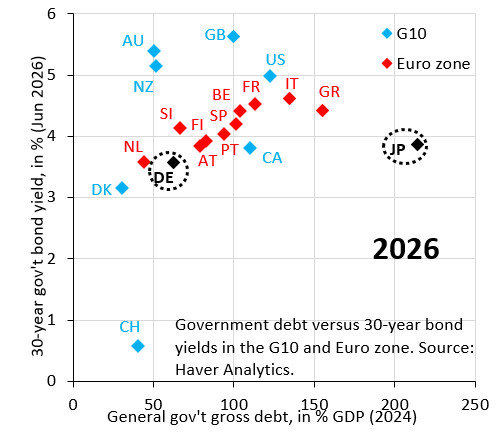

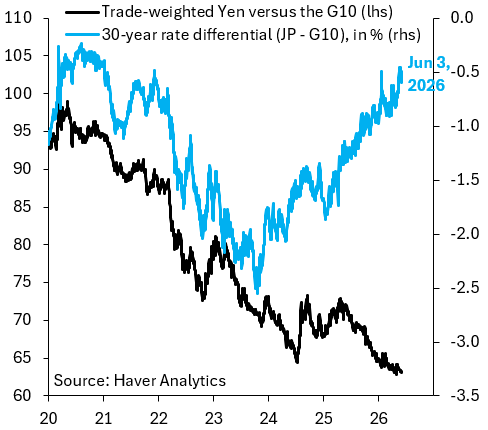

Let me start by outlining my position. In my opinion, Japan’s basic problem is that its long-term government bond yields are being kept artificially low by ongoing - and big - purchases of government bonds by the Bank of Japan (BoJ). The chart above shows how big this distortion is. Gross public debt is 240 percent of GDP, almost four times as high as Germany, but the 30-year government bond yield for Japan is basically the same as Germany. This means a fiscal risk premium, which would show up if the BoJ stopped buying government bonds, is being artificially suppressed, which is what’s putting depreciation pressure on the Yen. The BoJ is aware of this, which is why it’s reducing the pace of its bond buying in an attempt to let yields rise. But - because it’s likely that “true” yields are substantially above current yields - the BoJ has to do this very slowly and carefully, which - as the chart below shows - is what’s giving us the counterintuitive pattern whereby the 30-year yield differential of Japan versus its G10 peers is rising, which should lift the Yen, but the Yen is falling. That’s a signal - in my view - that observed yields are far below where markets would set them without BoJ interference. What would be a bond market crisis without the BoJ has morphed into a currency crisis. One way or another, Japan’s debt overhang is making itself felt.

What Japan needs to do to get out of this debt trap is have the government sell some of the financial assets it holds to pay down public debt. These holdings are huge and are the reason net debt is only 130 percent of GDP. That’s still high, but it’s a heck of a lot lower than 240 percent of GDP. This is where Brad’s views come in. Because net debt is so much lower than gross debt, my sense is that he doesn’t think there’s a debt problem. Therefore, it’s perfectly reasonable for Japan to use its official FX reserves to periodically intervene to stop the Yen from falling. Brad like to point out that Japan is doing these interventions at a profit, because it’s selling Dollars it bought when the Yen was much stronger. I disagree on two front. First, Japan isn’t a hedge fund. The objective isn’t to make profitable FX interventions. The goal is to sustainably stabilize the Yen. Only debt reduction can do that. Second, while it’s true that net debt is a lot lower than gross debt, this hardly matters if the government isn’t willing to mobilize these resources to pay down gross debt. The signal we’re getting so far - a signal that grows with every round of FX intervention - is that Japan isn’t ready yet to do that. If that’s true, only gross debt matters and net debt - at this point - is academic.

This brings me to Joe’s argument. Joe says that - by selling its FX reserves - Japan is doing exactly what I’m advocating, i.e. it’s selling its financial assets - in this case its holdings of US Treasuries - and presumably using the Yen it buys to pay down debt. While that’s true, in my opinion the signal’s all wrong. The signal Japan needs to send is that it recognizes debt is a problem. It can do that with a wave of privatizations and sales of domestic assets. In my view, markets would reward that with a stronger Yen and lower yields, i.e. exactly what Japan needs. FX interventions signal exactly the opposite. They signal denial, with the government papering over the symptoms of the debt overhang with FX intervention instead of confronting the problem. The market punishes this denial with continued depreciation pressure on the Yen. The signal is the wrong one because Japan has yet to reach “acceptance.”

So my disagreement with Brad and Joe is on the underlying root cause of what’s going on and - therefore - what needs to be done to fix things. It’s true that intervention has worked to cap $/JPY at 160, but the half-life of intervention is falling rapidly. In my opinion, Japan risks ending up in a place where intervention no longer stabilizes the Yen, which is when the real nightmare starts. Better to avoid that.

The argument proposed by Robin seems intuitive. As I understand it the BOJ is buying JGBs in mass, thus keeping rates low but flooding the market with currency thus weakening JPY. Simultaneously, the MOF is issuing JGBs and buying JPY. Complete lunacy but totally consistent with my experience with the tatewari nature of the GOJ. The Japan as hedge fund concept is fun to think about but can’t image the conservative bureaucracy would let this happen except through sheer incompetence which I think they are not. The root cause is the obvious: too much debt and that is a political problem. And it’s getting worse not better.

Mr. Robin Brooks,

I fully agree to your views.

The attached below is my Monthly just uploaded to my Ameblo.

I hope it will be of your help.

Thank you very much for your interest in Japan problems.

Tomo Nakamaru

Former World Bank Economist

🌐 June 2026 Global Markets Monthly

A Turning Point in U.S.–Japan Monetary Policies: The End of High-Pressure Economics and the Rise of “Loss of Control Risk”

1. Two Realities Emerging in June Markets

Global markets have entered a decisive turning point.

Last night, U.S. financial markets reacted with a classic hawkish shock:

U.S. long-term yields rose again

Equities declined

The dollar strengthened, pushing USD/JPY into the 160-165 range

These moves were driven by:

Strong May ADP employment data

A hotter ISM services inflation component

The Fed’s Beige Book highlighting resilient demand and labor markets

The Walsh-led Federal Reserve’s clear commitment to price stability above all else

Meanwhile in Japan:

Governor Ueda’s Kisaragi-kai speech signaled a shift toward rate hikes

Yet the yen continued to weaken past 160

WTI crude resumed its rise, amplifying Middle East risk

The gap between policy intentions and market realities has widened sharply.

2. United States: The Walsh Fed Signals Serious Inflation Control

From the outset, Chair Kevin Walsh has made it clear that inflation control is the Fed’s top priority.

Market reactions now reflect a renewed understanding:

The Fed is not in a hurry to cut rates — and may even keep the door open to further tightening.

The U.S. economy still retains buffers that make a soft landing possible:

Strong labor market

Healthy household balance sheets

Solid corporate earnings

Deep and resilient financial markets

A policy rate already high enough to anchor expectations

3. Japan: Ueda’s “Too-Late Normalization” and Its Dangers

In his June 3 speech, Governor Ueda stated:

“Real interest rates remain extremely low as underlying inflation approaches 2%.” “If upside inflation risks rise, the Bank must discuss the need for rate hikes.”

This effectively signals a June rate hike.

But the problem is simple:

Japan is tightening far too late.

Three risks from a delayed and small rate hike:

Yen carry unwinding → sudden yen rebound → equity sell-off

Fragile JGB market → nonlinear jump in long-term yields

Regional banks & insurers → unrealized losses → credit tightening

A rate hike may fail to curb inflation — yet still trigger asset price instability.

4. Yen at 160: A Structural Loss of Confidence

The yen’s slide past 160 is not merely about rate differentials.

It reflects a deeper market judgment:

“The BOJ cannot control inflation.”

As argued in my May Monthly Report: With deeply negative real interest rates, inflation becomes unanchored.

This creates a self-reinforcing cycle:

Yen depreciation → higher inflation → lower real rates → further yen selling

A classic arbitrage loop.

5. Sanae-nomics and the Failure of High-Pressure Economics

Sanae-nomics — essentially a “double-down” version of Abenomics — relied on:

Fiscal expansion

Yen depreciation

Equity market prioritization

Prolonged monetary easing

But this high-pressure approach eliminated Japan’s policy flexibility.

The consequences:

JGB market remains dependent on the BOJ

Financial institutions cannot withstand higher rates

Yen depreciation fuels imported inflation

Real wages stagnate

Consumption weakens

Equity prices rise only because of the weak yen

A stagflationary bubble has formed.

6. The Shadow of a Third Oil Shock

WTI crude is rising again. U.S.–Iran negotiations under the Trump administration remain uncertain. Middle East risk is intensifying.

Ueda himself warned:

“Higher oil prices can easily spill over into core inflation.”

Japan — with its extreme dependence on imported energy — is among the most vulnerable economies.

7. Conclusion: Japan Stands at the Edge of “Loss of Control Risk”

Under the Walsh Fed, the U.S. is restoring policy credibility and preserving room for maneuver.

Japan, by contrast, faces:

A delayed rate hike cycle

A distorted bond market

Fragile financial institutions

Yen-dependent equity valuations

Persistently negative real interest rates

Japan is now entering a phase where:

Raising rates is dangerous. Not raising rates is also dangerous.

This is the hallmark of a country that has lost policy freedom — and is approaching a genuine loss of control risk.

The June BOJ meeting will be a decisive turning point for Japan’s economic trajectory.