Embargo Iran

The fastest way to reopen the Strait of Hormuz is to stop Iran's oil exports

The single biggest failure of the Biden administration is that - in confronting Russia over its invasion of Ukraine - it feared that forceful action on sanctions could cause a spike in oil prices that might result in the Democrats losing the 2022 midterms. A full embargo of Russian oil would certainly have spiked oil prices, but we don’t know how long such a spike would have lasted. An embargo would have pushed Russia into deep financial crisis. The Ruble would have gone into a devaluation spiral, inflation would have soared and economic activity would have collapsed. We don’t know if this would have ended Russia’s murderous invasion of Ukraine, but it’s really hard to fight a war when your economy is imploding.

Instead, here we are over four years later. Russia’s war machine grinds on in Ukraine and - thanks to the recent spike in oil prices - Putin is reaping a large windfall on top of that. The basic mistake in 2022 was to fear temporary disruption in oil markets, for which we’ve been paying the price ever since in the form of an emboldened Russia. In global geopolitics, as in economics, there’s no free lunch. Biden pulled his punches in 2022 and we’re dealing with the consequences over four years later.

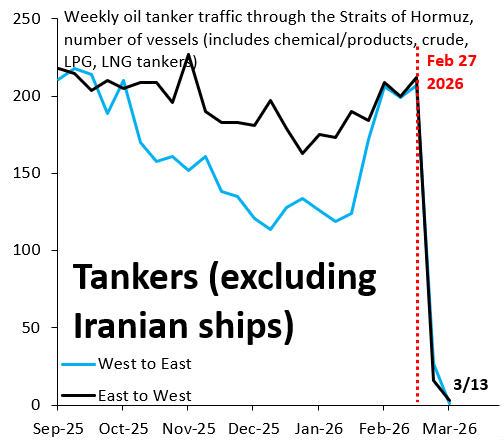

The Trump administration is now in danger of falling into the same trap. Oil tanker traffic through the Strait of Hormuz - excluding ships carrying Iranian oil - has all but ceased, as the chart above shows. Meanwhile, the Wall Street Journal reports that Iran’s oil exports have risen as it exploits a global supply shock that has countries like India clamoring for oil. The Trump administration is turning a blind eye to this, because it fears that shutting down Iranian shipments will further spike oil prices. That’s exactly the wrong calculus and repeats the basic error Biden made.

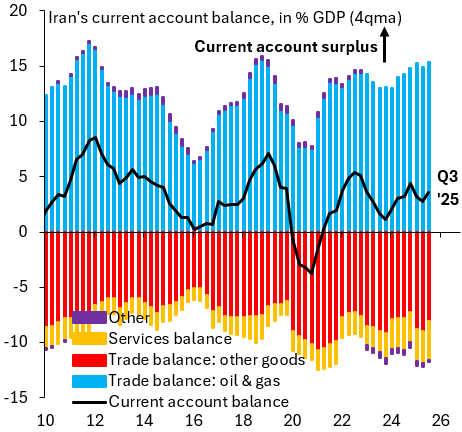

Instead, the US should announce a blockade of all ship traffic in and out of Iran’s ports. Given the huge presence of the US Navy in the region, no shots would have to be fired. Remaining tanker traffic in and out of Iranian ports would cease right away. This would push Iran’s economy into deep crisis. As the chart above shows, oil and gas exports currently amount to around 15 percent of GDP (blue bars). This would go to zero overnight, as would Iran’s ability to pay for imports (red bars). The economy would implode and - with it - the Ayatollahs’ already shaky hold on power.

Which brings us to oil prices. The key unknown in this conflict is how long the Strait of Hormuz stays shut for Western oil tankers. As markets raised their guess for how long it stays shut in recent weeks, the Brent oil price has risen. An embargo of Iranian oil, if the collapse in Iran’s economy is deep enough, could convince markets that the closure of the Strait might end sooner rather than later. As a result, Brent might only spike briefly or even fall. More importantly, an embargo might help avoid the Ukraine scenario, where an emboldened Russia wreaks havoc four years after the invasion. An embargo would “trade” temporary oil market disruption for higher odds of genuine regime change in Iran. The Trump administration would avoid repeating Biden’s mistake into this year’s midterms.

What you seem to be missing is that Iran’s ability to endure hardship is far greater than the ability of global financial markets to absorb sustained pain—not to mention the political cost the U.S. administration would pay through higher inflation and slower economic growth.

Bloodlust is the last refuge of the failed market prognosticator.

Am I the only one who has noticed that this Substack writer bizarrely pivots to militaristic (or quasi-militaristic) solutions to support his political preferences when things are not going his way?

As an occasional reader of this newsletter — occasional because he writes too much and like a heavy blizzard buries you in such a snowdrift of words that most of us struggle to remember what his views were a week ago, never a month or a year ago — I have noticed that he has been getting a lot of things wrong. The best solution to that sort of repeated failure is to change the subject, a kind of chicanery.

So tariffs in 2025 were supposed to create inflation in the US and disinflation in the export countries, US yields would rise, the US dollar would strengthen, etc,( yet all talk of the dollar’s diminished standing as a reserve currency was bunk.) Well, we know what happened to the dollar against all the major currencies (except the yen) in 2025.

When predictions falter, bait and switch. Monetary debasement becomes the dominant theme in late 2025. All government yields every are going to rise because of fiscal incontinence. Did not happen. Then bait and switch again. Era of the strong dollar is over, and a dollar crisis is coming. The currency will be fall sharply against its peers.

But history has a nasty habit of intervening and kicking the legs out under one’s fondest hopes. Oil experiences a historic surge because of the US and Israel’s foolhardy warmongering. And of course the dollar goes exactly in the opposite direction — not because of all this triumphalist nonsense that Wall Street hucksters like Brooks and his fellow-travelers from investment banks have been peddling — of a “flight to safety” and “flight to quality” — but because the $ has been the carry currency of choice for the last many years. Investors have been short the dollar for years, so when a geopolitical shock hits, there is an unwinding of these unhedged positions and there is a “flight to home”, which is the correct way to see it.

So that’s when a descriptive accounts of the market become prescriptive ones, even though they are totally inconsistent. So hit the Russian shadow fleets and reduce the supply of oil in global markets (because Ukraine matters a lot to the author of this newsletter) but hit the Iranian oil hubs and increase the supply of oil (because Israel matters to him equally).

In the end, we get a tangled web of nonsensical predictions and opinions from him.