Is US inflation picking up?

There's NO sign underlying inflation is picking up despite yesterday's "hot" CPI

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

One of the themes I write about a lot is rising long-term interest rates as markets fret about fiscal policy running out of control across so many advanced economies. In my opinion, higher long-term yields are about markets demanding insurance against the risk that governments will at some point in the future try to inflate away the value of their debt by printing money. Now imagine how much more acute those market fears might be if inflation were already running hot. This is where yesterday’s CPI print for April comes in, which - on the surface - looks quite worrying.

I should clarify upfront that I’m an inflation “dove.” It feels to me like we’re on the cusp of a major automation wave in white-collar jobs that are heavily administrative and repetitive. There’ll be lots of people chasing far fewer jobs in coming years, which will put downward pressure on wages. I just can’t see how - with that as a backdrop - underlying inflation has room to pick up, even with everything that’s going on now.

But every new CPI print is a chance to kick the tires and that’s what I do in this post. Although yesterday’s data look worrying on the surface, I see no sign that underlying inflation is picking up. Once you filter out the noise, yesterday’s data show inflation running at the same pace as always since the end of the COVID shock.

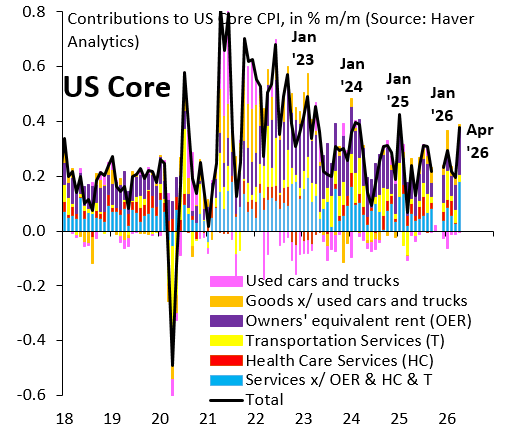

The chart above shows how I look at core CPI. The whole rationale for core inflation in the first place is to eliminate noise by dropping food and energy items. But this still leaves tons of stuff in core that’s either very noisy or imputed, i.e. not based on market prices. The blue bars show my “core” services metric, which pares core CPI down even further to create what I think is a good measure of underlying inflation. This measure drops owners’ equivalent rent (OER), healthcare (HC) and transportation (T) from core services inflation. In April 2026, inflation in this category ran at its fastest clip since March 2022, i.e. since the immediate aftermath of COVID. That’s worrying.

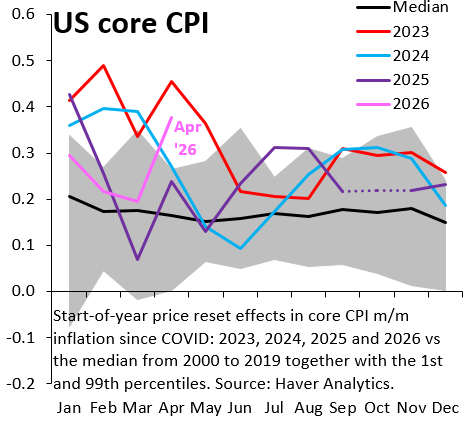

What’s also worrying is that you can’t dismiss rising core inflation with my favorite explanation of recent years: residual seasonality. As the chart above shows, residual seasonality has tended to push up core inflation in January and February, but this source of inflation is usually fading by the time April rolls around, so this isn’t a mitigating factor either.

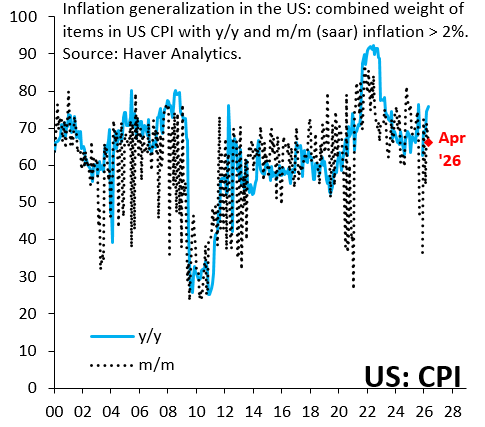

When all else fails, I fall back on my inflation generalization indices, which track the combined weight of items in the CPI with inflation above two percent. If underlying inflation is rising, the combined weight of items with inflation above two percent will increase. If “hot” CPI readings are mostly about noise, i.e. a few “hot” items here and there, this stuff should cancel out and the combined weight of items with above two percent inflation will be flat. It’s the latter that seems to be going on. I calculate the combined weight of items based on year-over-year (blue) and month-over-month (black) inflation for all the stuff in the CPI. This index based on month-over-month inflation is down in April 2026 from the month before and completely in line with readings since the COVID inflation shock faded. There is no sign that inflation is picking up. Yesterday’s “hot” CPI therefore belongs in the “noise” category.

The filtering methodology is rigorous but the question it answers is narrower than the question most investors are asking right now.

Stripping out OER, healthcare, and transportation removes the three categories where inflation is accelerating fastest. OER is a third of CPI. Transportation captures the Hormuz energy pass-through. Healthcare captures the insurance premium increases driving consumer distress. The remaining core services measure probaly does reflect stable underlying price pressure. But stable inflation in the components you kept and accelerating inflation in the components you removed produces a headline number that consumers and the Fed both have to respond to regardless of whats driving it.

The AI deflation thesis is the longer-term argument worth engaging with separately. If white-collar automation genuinley compresses wages over the next 3-5 years that is structurally deflationary. But the timing mismatch matters. Hormuz-driven energy inflation is hitting the economy now. AI-driven wage deflation is a 2028-2030 phenomenon at the earliest. The Fed has to set policy for the inflation thats arriving this quarter, not the deflation that might arrive in three years.

The honest synthesis is probaly that underlying inflation is stable AND headline inflation is accelerating AND both things are true simultaneously because theyre measuring different layers of the same economy. The question for positioning is which layer the Fed responds to, and historically the answer is headline.

Largest year over year increase in Core PPI in five years.

Nothing to see? PPI feeding into CPI ?