Learning About Kevin Warsh

Warsh made his second public appearance as Chair yesterday - patterns are emerging

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

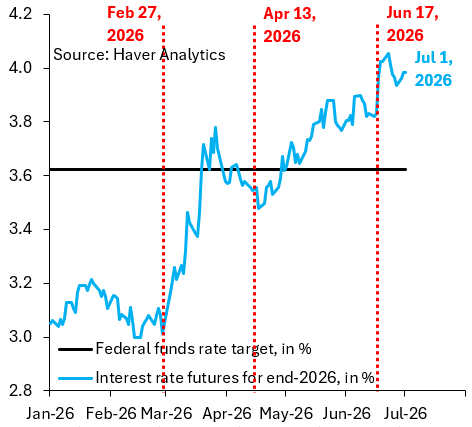

Markets had an unambiguously hawkish reaction to the Fed meeting two weeks ago, which was Kevin Warsh’s first public appearance as Chairman. Two things drove that reaction. First, Warsh repeatedly emphasized price stability and the fact that inflation has been above target for many years. Second, the “dots” in the Statement of Economic Projections shifted meaningfully in a hawkish direction. Where previously the median dot pointed to cuts, the June meeting suggested a growing willingness to hike.

As far as the dot plot goes, there’s two possible explanations for what happened. One is that the dots were stale, i.e. they didn’t incorporate the sharp drop in oil prices that had played out in the days leading up to the FOMC. In my opinion, that’s quite likely. After all, the President only signed the peace deal on June 17, i.e. the same day as the FOMC press conference. Another explanation - more of a conspiracy theory really - is that the hawkish shift in the dots is trying to box Warsh into hikes that’ll then get him in trouble with the President. If there’s any truth to this theory, it’s certainly worked. Markets went from pricing 20 basis points in hikes for this year the day prior to the meeting to 40 basis points the day after.

None of us really know what kind of Fed Chair Warsh will turn out to be. Yesterday was his second public appearance in this role and in my opinion something important happened. Asked if he thought markets were right to give a hawkish interpretation to the meeting two weeks ago, his answer was that “expectations of future inflation have come down in recent weeks and overall inflation risks have declined.” This very much leans in the direction that the dots were stale and that markets read too much into them.

All that said, as the chart above shows, markets did nothing to take back the hikes they price for this year. How is that possible? In my opinion, that’s due to a pattern that’s emerging. Warsh wraps everything he says in hawkish rhetoric, including with his frequent references to price stability. That sounds hawkish and is what gets picked up in reporting, like in this Reuters story. But this language is mostly performative. As I discussed in this past Saturday’s live stream, Warsh is working hard to establish his credibility and independence from the White House. The only way he can do that is to sound hawkish. Better to ignore all that and focus on his true message. That message was dovish yesterday.

Warsh does not have an easy job. This hawkish stance is understandable for 3 reasons: 1) the market thinks he is Trump's guy. So he had to build up credibility. He could do it cheap because oil prices went down already, 2) we still have 3% core inflation and communication a dovish stance with the Fed track record would be a mistake, 3) he has to manage the long end and he did that nicely.

I bought US corporate bond !! bet on the rate cut due to the increase of white-collar laid off and decrase of purchase power.