The Dollar falls to a new low

Truth versus myth in the ongoing depreciation of the US Dollar

In yesterday’s post, I wrote about what we know (and don’t know) about Trump 2.0. We know that the nexus of global markets and China is perhaps the only meaningful constraint on this administration. China’s Yuan devaluation right after Liberation Day sparked instability in the US Treasury market, which ultimately caused the President to backtrack on reciprocal tariffs one week after their announcement. The fact that this constraint exists is good and - in the eyes of most market participants - means that the trade war is essentially over.

Among the things that we don’t know - and there are many - perhaps the most important one is that no one knows where President Trump stands on Russia, i.e. is Putin friend or foe. Uncertainty around this question is in my view the main reason the Dollar has fallen in the face of tariffs (counter to the predictions of any economic model). After all, if the US makes nice with Russia, what prevents it from making nice with China? It is this uncertainty that’s preventing markets from pricing tariffs - since they may be lifted at a any moment - and is why the Dollar hasn’t risen as it should.

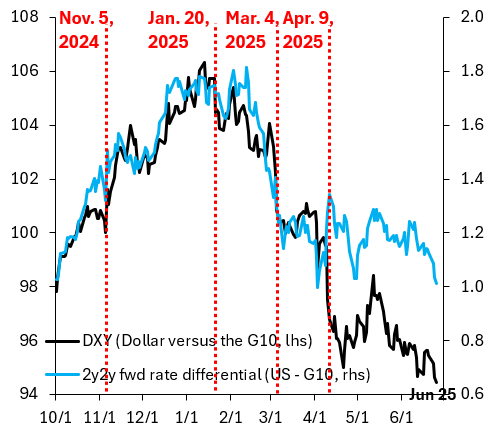

All that said, the Dollar keeps falling and made a new post-election low yesterday, as the black line in the above chart shows. Unlike early April, when the Dollar fell even as the interest differential rose (a deeply alarming confluence), the fall in the Dollar now is entirely ordinary and unremarkable. That’s because interest differentials are moving against the Dollar (blue line). Markets believe the Fed will be more dovish than its G10 counterparts, which is what keeps dragging the Dollar lower.

As I’ve noted in previous posts, I disagree with this logic. Tariffs are inflationary for the US, but deflationary for the Euro zone and other net exporters. This divergence in inflation - for which early signs are already apparent in the global manufacturing PMIs - is something that should move rate differentials in favor of the Dollar, not the other way around. Markets aren’t there yet, mainly because recent inflation prints have been downside surprises. As I’ve laid out, these downside surprises are about to end, which should also spell the end of Dollar weakness.

News are coming that Trump will name new FED chair in the summer. As he will be politically dependent, he will act as a shadow chair. Hence, no matter what happens to inflation, markets are pricing lower fed fund rates.

What is the logic of higher inflation leading to a stronger dollar in a political environment in which the Fed will be pressured to lower interest rates?