Broad Dollar Weakness

Once the war officially ends, the Dollar will start tumbling

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

When I still worked for Goldman, I’d travel endlessly around the country to present the firm’s outlook for foreign exchange rates. In one of those meetings, just as I pulled up the cover slide of my PowerPoint presentation, the entire room burst out laughing and - for the life of me - I couldn’t figure out why. After I’d plodded through my slides, someone took me aside and said: we laughed when you got started because your cover slide always has the same title, i.e. “Broad Dollar Weakness.”

The years after the global financial crisis were a time of profound Dollar weakness because the Fed was way more dovish than its peers. This had caused me to fall into the unfortunate habit of keeping my cover slide unchanged as I updated the rest of my presentation. I was mortified and retired the “Broad Dollar Weakness” cover slide right after. That was just as well because the Dollar started a massive appreciation cycle around a year later.

When I laid out my forecasts for 2026 in a post on January 1, my key expectation was for “Broad Dollar Weakness.” The war with Iran has temporarily disrupted this, but - as markets grow increasingly confident that some kind of deal is coming - the Dollar has resumed its fall. Indeed, given how aggressively markets are already selling the Dollar now, I think the Dollar might really tumble once we get an actual peace agreement.

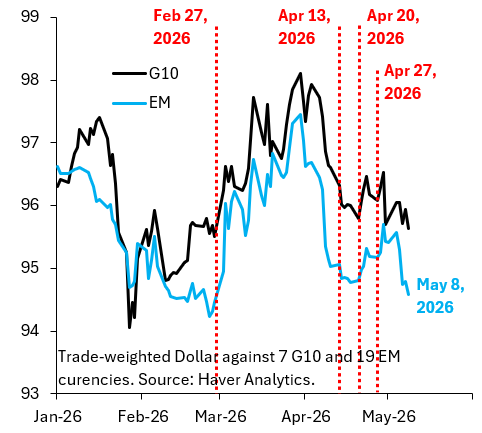

The blue line in the chart above shows the trade-weighted Dollar versus 19 emerging markets (EM). This is in my opinion the single best barometer for Dollar sentiment in markets and we’ve just fallen back to pre-war levels, even though we’re nowhere near an actual peace agreement. My interpretation of what’s happening is that markets are extremely Dollar bearish. They know they need to trade their view ahead of an actual peace agreement, so they’re doing that now and willing to bear the pain of a few false starts. That to me feels like a high conviction view and suggest that the Dollar could really start to tumble once we get an actual peace agreement.

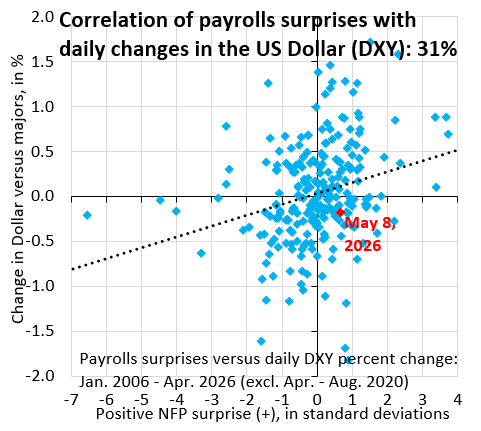

There’s another (nerdier) reason why I think we’re heading for “Broad Dollar Weakness,” which is that the Dollar is no longer rising on positive data surprises. The chart above shows yesterday’s upside surprise to payrolls on the horizontal axis and the response of the Dollar on the vertical axis. Historically, yesterday’s upside surprise should have been worth some rise in the Dollar, but instead it fell. This is how the Dollar traded in the years after the global financial crisis, when I’d grown too lazy to update my cover slide. We’re seeing a regime shift unfolding, whereby positive data surprises see the Dollar weaken. That’s a big deal.

My bottom line is simple. If markets are trading Dollar weakness as aggressively as they are now without an actual peace agreement, things will really get going once the war officially ends. The best way to trade this is versus EM. The Brazilian Real, which I’ve flagged as one of the main beneficiaries, keeps making new highs in recent days against the Dollar. I expect that to continue.

Interesting and forward looking.

QT UNDER WARSH COULD BE ANOTHER STORY