Is the Case for Dollar Weakness Over?

Dollar weakness will resume once markets realize that the Fed isn't going to hike

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

One of my forecasts for 2026 is that the Dollar will fall around 10 percent on a broad, trade-weighted basis. In the first few weeks of the year, it certainly seemed like this was the right view, with the Dollar falling over two percent in January on all the noise around Greenland, but the war with Iran changed all that. We’re back to flat now and - with all the chatter about Fed hikes - this post kicks the tires on my Dollar view.

Recent Dollar strength has two sources. First, the war with Iran has increased the degree of risk aversion in markets. That’s led to safe haven buying, which has lifted the Dollar. Second, markets have switched to price hikes from the Fed, in part because they think high inflation will force its hand. The first source of USD strength will fade as soon as we get a peace deal. I have no visibility on when that’ll happen, but this war is by definition temporary. The second misreads US inflation. I’ve been emphasizing for some time that there’s no indication of overheating in any of the inflation data and yesterday’s CPI confirmed this. All this means that I’m sticking with my Dollar down view. An end to the war and markets going back to pricing Fed cuts is worth a five percent drop in the Dollar. We’ll get there soon enough.

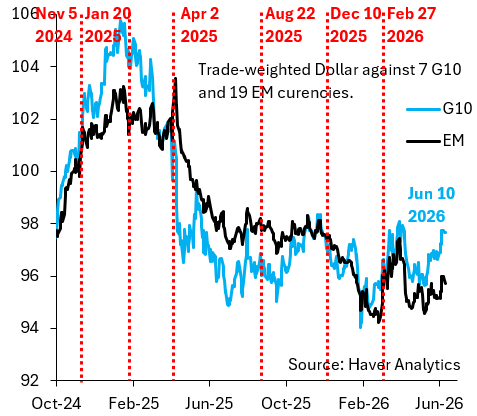

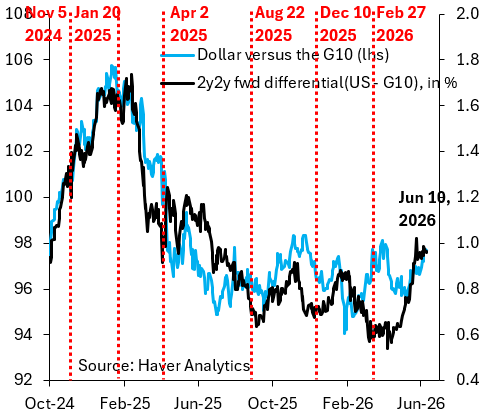

The blue line in the chart above shows the trade-weighted Dollar against seven of the G10 economies, while the black line is the Dollar versus emerging markets (EM). Year-to-date, the Dollar is up 1.5 percent against the G10 and down 0.9 percent against EM. I see the Dollar versus EM as a much better leading indicator for how things are likely to develop, but it’s still worth looking into why the G10 Dollar has risen so much. The chart below does this. The blue line is the Dollar versus the G10 and is the same as in the chart above. The black line is the corresponding 2y2y forward rate differential of the US vis à vis the G10. Markets think the Fed has moved in a hawkish direction due to the war, the rise in oil prices and elevated inflation. More important, they think the Fed has become more hawkish relative to its peers. That’s why the G10 Dollar is up.

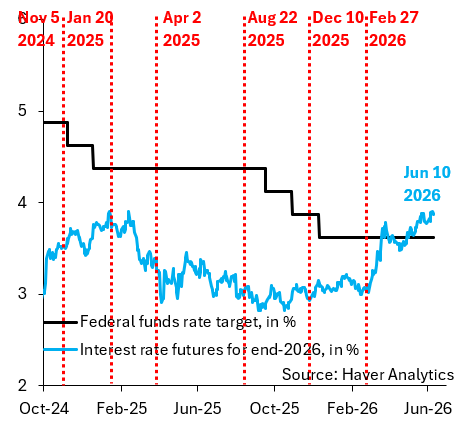

A simpler way of saying the same thing is that markets have ditched rate cuts, which they were pricing until the war with Iran began. They now price Fed hikes, as the chart below shows. What’s odd is that they’ve stuck to their guns on this even as oil prices are have fallen lots from their highs in March and April. My best interpretation for why they’re doing this is that they’re misreading US inflation, which - in contrast to what markets think - is well-behaved, something yesterday’s CPI underscored.

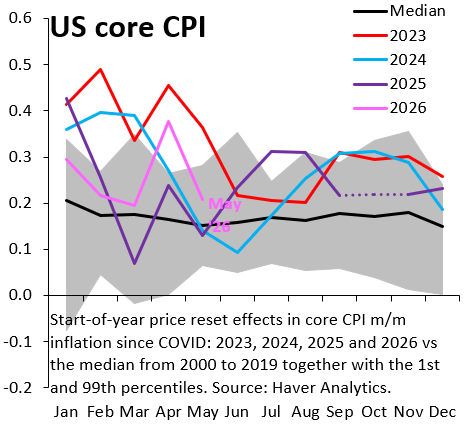

There’s all kinds of noise in US inflation data since COVID, in part because the quality of seasonal adjustment has fallen, so I use the chart below as one gauge for what’s going on. It shows the pace of month-over-month inflation throughout recent calendar years. Nominally, these data are seasonally adjusted, but - as the jumps at the start of 2023 and 2024 show - there’s lots of residual seasonality since COVID that’s messing things up. The point of this chart is that - once you cut through all this noise - yesterday’s CPI reading was very benign, as the pink line shows. That’s in line with all the work I do tracking inflation, which doesn’t show signs of overheating.

My bottom line is that Dollar strength is temporary. The end of the war will cause safe haven flows to reverse, driving the Dollar weaker. In addition, falling oil prices will change people’s minds on the Fed, reminding them that underlying inflation is very well-behaved. These two things alone - in my opinion - are worth a five percent drop in the Dollar, which will happen quickly if and when we get a peace deal.

the hundred years war was temporary

I tend to agree, Robin. The issue is the new Fed chair and what that means for markets .. along with other currencies being far from reliable and over positioned.. such as AUD, and the JPY.. which we both agree .. is structurally unsound. There is also the persistent USD demand from US tech .. or for US tech. Once Warsh is in, and confirms he is dovish … the USD will weaken.