Inflationary pressure from tariffs mounts

Rising US inflation would be a game changer for the Dollar and trade negotiators

Earlier this week I met with a delegation from a large current account surplus country that’s trying to negotiate a trade deal with the US. One of the main questions they had was about US inflation and whether tariffs will push it up. Rising inflation would put US negotiators on the defensive - so this team hoped - and make it easier to reach a deal along the lines of what the UK was able to negotiate.

The inflation outlook is of huge importance to trade negotiators and the Dollar, which - as I outlined yesterday - has fallen largely for cyclical reasons, with markets thinking the absence of inflation allows the Fed to be more dovish than other central banks. As I’ve also noted previously, there are clear signs from the global manufacturing PMI’s that inflationary pressure is mounting in the US, with firms reporting they’re passing on more price increases to customers. At the same time, China is aggressively using transshipments to avoid paying tariffs, which may be delaying any rise in inflation.

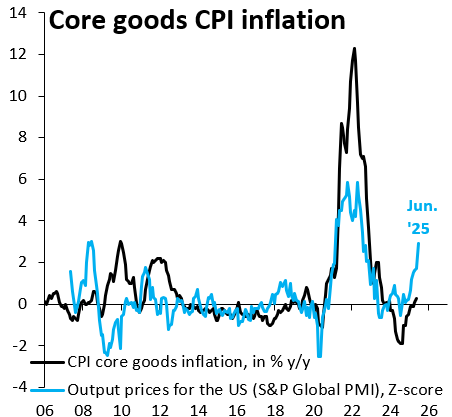

So how do all these various things stack up? The black line in the chart above shows year-over-year core goods inflation. This category has a weight of 25 percent in core CPI and excludes food and energy commodities to focus on underlying inflation. The blue line shows the S&P Global series for output price inflation in the US, which I’ve highlighted in my previous discussions of the global manufacturing PMIs. It’s clear that inflationary pressure is rising based on S&P Global data and it’s also clear that this is not yet translating into actual goods price inflation.

Why this divergence? The most obvious reason is that S&P Global data are based on surveys. These kind of sentiment data have an “emotional” element that may overstate what’s going on with actual inflation. Having worked with these kind of surveys a lot during COVID, when they correctly predicted the inflation surge, I am skeptical of that argument though. When something big is happening, as was the case back then and is the case now, surveys accurately picked up rising inflationary pressure. Another reason might be that these survey data tend to lead actual rises in inflation by a couple of months. There’s some evidence of this historically, which means that higher US inflation is in the pipeline. After all, this administration has only been in office for five months and tariffs have been in place for less than that.

What it all comes down to is that inflationary pressures are rising and that factors holding down inflation are temporary. I expect core PCE inflation to be rising 3.5 percent year-over-year in Q4 of this year, which will keep the Fed on hold, support the Dollar and help foreign trade negotiators.

You are a brave man, RJB.

I am reading and watching the progression of your thinking. Thank you.