Requiem for $200 Oil

There's a lot to learn from the fact that oil prices didn't go to $200

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

Perhaps the single most important thing about the last few months is what did NOT happen: oil did not go to $200 a barrel, even though there were many voices who told us - over and over - that this was imminent. There’s important lessons in that. Today’s post summarizes why I think $200 didn’t happen and what the policy implications are.

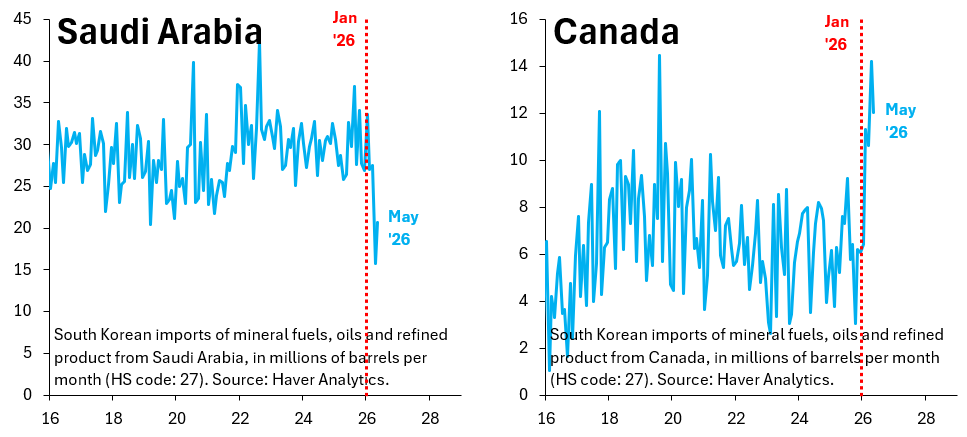

In my mind, there’s two principal reasons why we didn’t go to $200. First, academic estimates for the price elasticity of demand have turned out to be largely correct. As I laid out in March and discussed with Paul Krugman on his podcast, those elasticities justified an oil price rise of 80 percent at most, which equates to roughly $125 a barrel and is where we more or less ended up at the worst moments in this shock. The case for $200 was therefore never really there. Of course, there’s people who now claim we only didn’t go to $200 because on-again, off-again peace talks avoided such a spike. I don’t think that’s right. There were no peace negotiations back in March and oil still didn’t manage to rise sustainably above $125. Second, the ingenuity and robustness of global oil markets has turned out to be far more impressive than apocalyptic forecasts implicitly assumed. I’ve given the example of South Korea, which - no surprise - saw its imports of oil from Saudi Arabia collapse during this shock. It pivoted to import lots of oil from Canada and other places, so that its overall oil imports barely fell. It’s true that South Korea had to “pay up” to import Canadian oil, but that’s exactly how markets are supposed to work. This “arbitraged” the Strait of Hormuz shock to places far afield, spreading it out and - thereby - making the global economy more resilient.

The policy implications from all this are immediate. The West pulled its punches on Russia back in 2022 because of concern that an outright blockade could lead to a big spike in oil prices that might drive the global economy into recession. Indeed, at the time there was one investment bank that had an oil price forecast of $380. We know this stuff is nonsense now thanks to the past few months. The closure of the Strait of Hormuz is a far bigger shock than blockading Russian oil could ever be. Russia’s oil exports out of the Baltic are about double what Iran was exporting before the US imposed its blockade. We’ve learned that a blockade can be done, that it adversely impacts the target country and - most importantly - that it doesn’t uncontrollably spike oil prices. The immediate lesson is therefore for Europe, which - if it doesn’t want to do an outright blockade of Russia in the Danish Straits - can easily clamp down on the shadow fleet. Ben Harris and I recently put out a proposal on this.

Let me now discuss the price elasticity point, the supply chain robustness point and the blockade in detail:

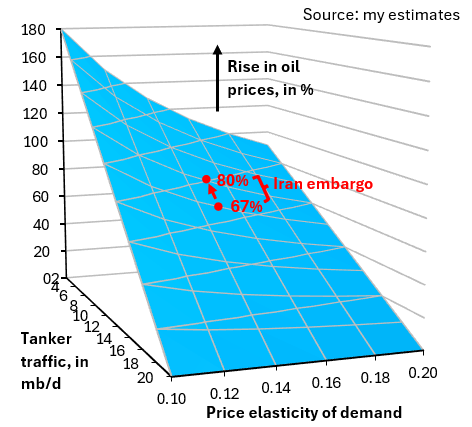

Academic price elasticity estimates have been validated: I made this chart for a post on March 19, which was right around the peak of the panic over oil prices. It shows that if oil out of the Persian Gulf is running at half its pre-war capacity due to encumberment of the Strait of Hormuz (10 mb/d on the axis going away from the reader), then reasonable estimates for the price elasticity of demand (around 0.15 on the horizontal axis) say oil prices should rise between 70 and 80 percent (the red dots on the vertical axis). The last couple of months have been a natural experiment of sorts and have validated this framework, which is just another way of saying that the midpoint of academic price elasticity estimates looks to be a good number to work with. I don’t think inventory depletion is a good pushback to this, nor is the idea that on-again, off-again peace talks prevented oil prices from going higher. After all, there were no peace talks in March and oil prices still failed to sustainably rise above the 80 percent threshold.

Global oil markets are incredibly resourceful and resilient: the two charts above update analysis I did in a post a few weeks ago. They show South Korea’s imports of oil from Saudi Arabia in the left chart. Those tumbled in April and recovered a bit in May. South Korea was able to almost fully offset this drop by ramping up imports from Canada as the right chart shows. This re-jiggering doesn’t lessen the underlying shock. The Strait of Hormuz is still just as closed as before. But it shows that the major industrialized countries were able to “pay up” to source oil and keep their economies going. This dispersed the shock and drove up prices in the US and Europe, averaging things out and making the global economy more resilient. That’s something $200 forecasts implicitly assumed wasn’t possible.

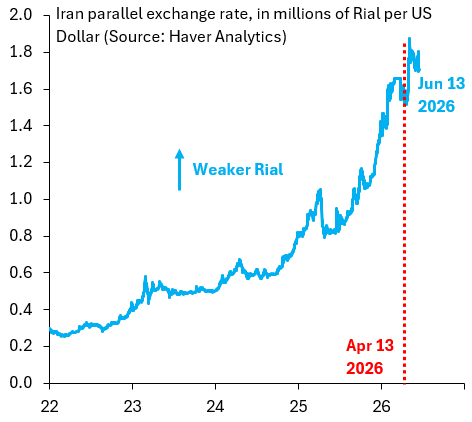

The US blockade of Iran worked: the chart above shows what little data we have for the Iranian Rial. Right after the start of the blockade on April 13, the Rial fell sharply against the Dollar, while it’s strengthened in recent days as the likelihood of a peace deal rose. That’s consistent with capital flight as soon as the blockade came into force, with Iranian residents seeking to convert their savings into the Dollar, while the reverse is happening now. Capital flight was also the first thing that hit Russia in 2022 after the West imposed sanctions. We’ll never know what role the US blockade played in getting the Iranian regime to negotiate, but its effects on the Rial are obvious to see and that’s before we’ve even talked about the loss in export revenues or Iran running out of storage for its oil.

The bottom line is that global oil markets are a lot more resilient than $200 forecasts implicitly assumed. That’s good news for Western policy makers, especially those in Europe. There’s still time to hit Russia by clamping down on the shadow fleet. The effects on oil prices will be modest and - as I have been flagging recently - there’s a lot of scope for the EU to boost sanctions enforcement.

The Law of Demand. I keep thinking of that these days. Price goes up, demand goes down; the measure of how much is elasticity. The simplest example is that South Asia cannot pay $200/bbl.

I see an even bigger refutation of the Law of Demand in AI. The market assumption is that AI consumption will continue to rise even as the price of token soars. Also, demand for GPUs, memory chips, electricity, etc., will continue to rise even as the prices for those inputs rise by 10X. That's almost impossible. Demand will fall, substitutes will be found, supply will increase-- the price will not persist.

I agree with this as we have seen much mitigation of the supply shock. Some of it is not sustainable and we will see what happens if it continues.

The other thing is that the vulnerability to a second shock is high during this period. A political upheaval in a major producer, a terrorist attack on major pipelines, a natural disaster in a major refining port, etc. etc. could push things into what is normally a pathological case.